CONTENT FROM: FINANCIAL PLANNING WEEK REPORT

PUBLISHED NOVEMBER 20, 2020

In a tough year, some loss of financial confidence among Canadians: planning holds the key

When FP Canada launched its first Cross-Country Checkup Survey in 2018 to gauge Canadians’ collective pulse on financial matters, it found a significant majority of survey respondents – almost seven in 10 – were confident in their ability to achieve their financial life goals.

What a difference two years has made.

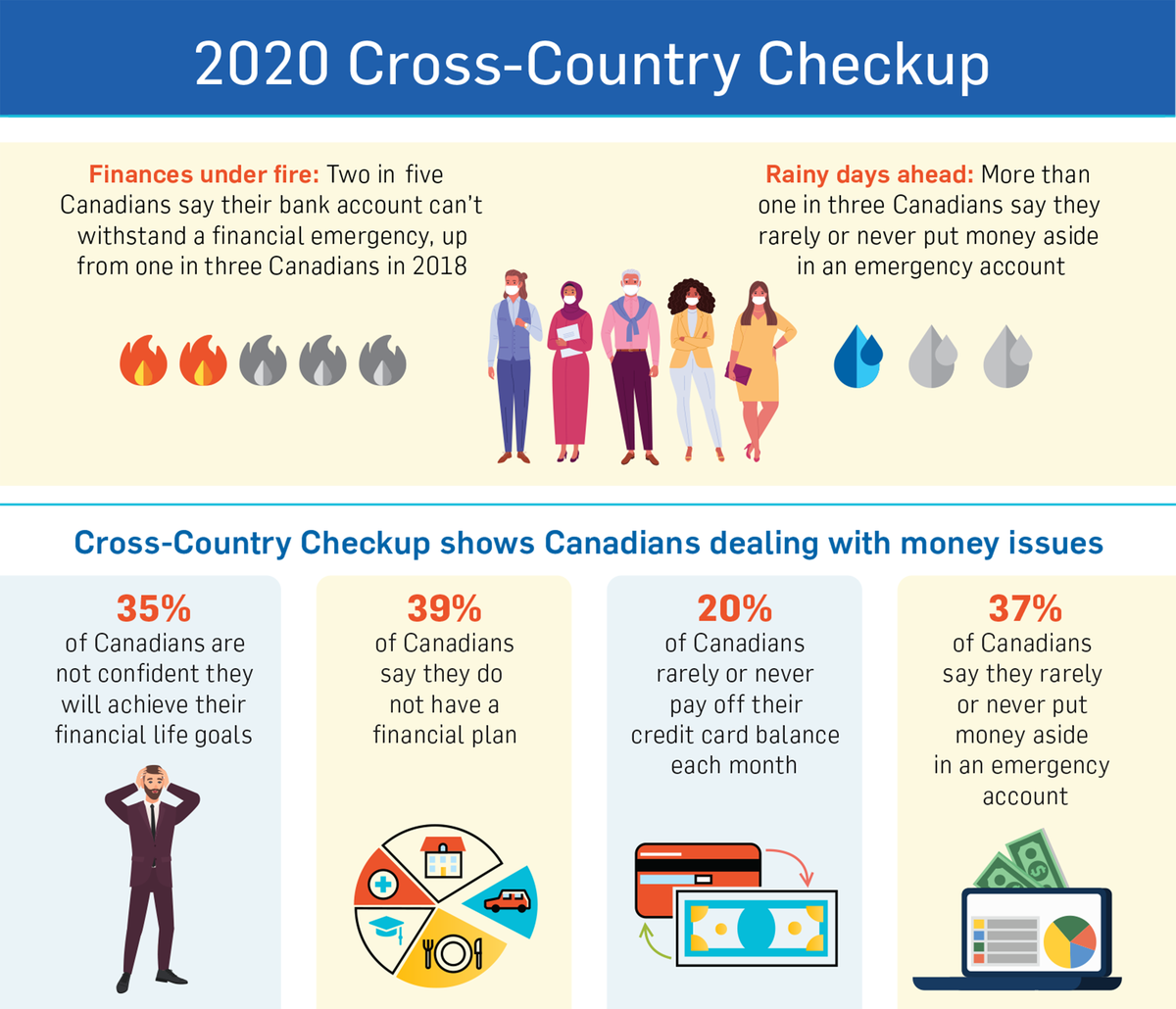

The FP Canada Cross-Country Checkup Survey conducted this September revealed a country less certain about its financial future. Of the 1,538 Canadians surveyed, 57 per cent said they were confident they would meet their financial goals, down from 67 per cent in 2018.

“This has been a particularly tough year because of COVID-19,” says Caval Olson-Lepage, a Certified Financial Planner at Affinity Credit Union in Saskatoon, Saskatchewan. “We’ve seen significant job losses and instability across Canada, so you have a lot more people feeling financially strained right now.”

That financial strain is reflected in FP Canada’s latest Cross-Country Checkup Survey. Nearly 40 per cent of Canadians say their bank accounts can’t withstand a financial emergency, up from 33 per cent in 2018.

The survey also sheds light on the financial well-being and mindset among various demographic groups. The Sandwich Generation – Canadians aged 45 to 54 years – were the hardest hit, with 53 per cent saying they couldn’t handle a financial emergency.

However, it isn’t all doom and gloom for Canadians. Three-quarters of Canadians who work with a financial planner feel more confident and say they can withstand a financial emergency. Yet today, more than 70 per cent of respondents say they have not engaged the services of a professional financial planner.

“The key to confidence is financial planning. When you have a solid financial plan in place, you have the confidence to make better decisions, and you’ll be better equipped to navigate challenging times,” says Scott Plaskett, CFP, CEO and senior financial planner at Ironshield Financial Planning in Caledon, Ontario.

Mr. Plaskett recommends a few simple tips:

- Automate savings by setting up a direct transfer from your chequing account to your savings account, as soon as the paycheque comes in.

- Use credit cards wisely. Select cards that offer cash back options and keep an eye on sign-up bonuses. Perhaps most importantly, pay off your credit card balance in full each month. Also make it a point to read your credit card bills to see where your money is going.

- When filing income tax returns, plan to save some if not all of your refund by putting it into an RRSP or a TFSA account.

Many Canadians continue to have misconceptions about working with a financial planner. The survey revealed 48 per cent of those who don’t work with a financial planner say they would if they had more money; 17 per cent said they weren’t sure where to find a professional they can trust, and 14 per cent said they didn’t know what questions to ask a financial planner.

Ms. Olson-Lepage suggests doing the research before choosing a financial planner. You want to look for someone who has the right credentials, understands your unique needs and is transparent.

Advertising feature produced by Randall Anthony Communications. The Globe’s editorial department was not involved.

Original Link: https://www.theglobeandmail.com/business/adv/article-cross-country-checkup-survey/

For more free information on Creating A Business Owner’s Dream Financial Plan, you can listen to a free, eight part series we did exclusively for business owners. The show is also available to subscribe to for free via iTunes.